The Buyer's Market Just Hit Its Peak. Most Investors Read It Wrong.

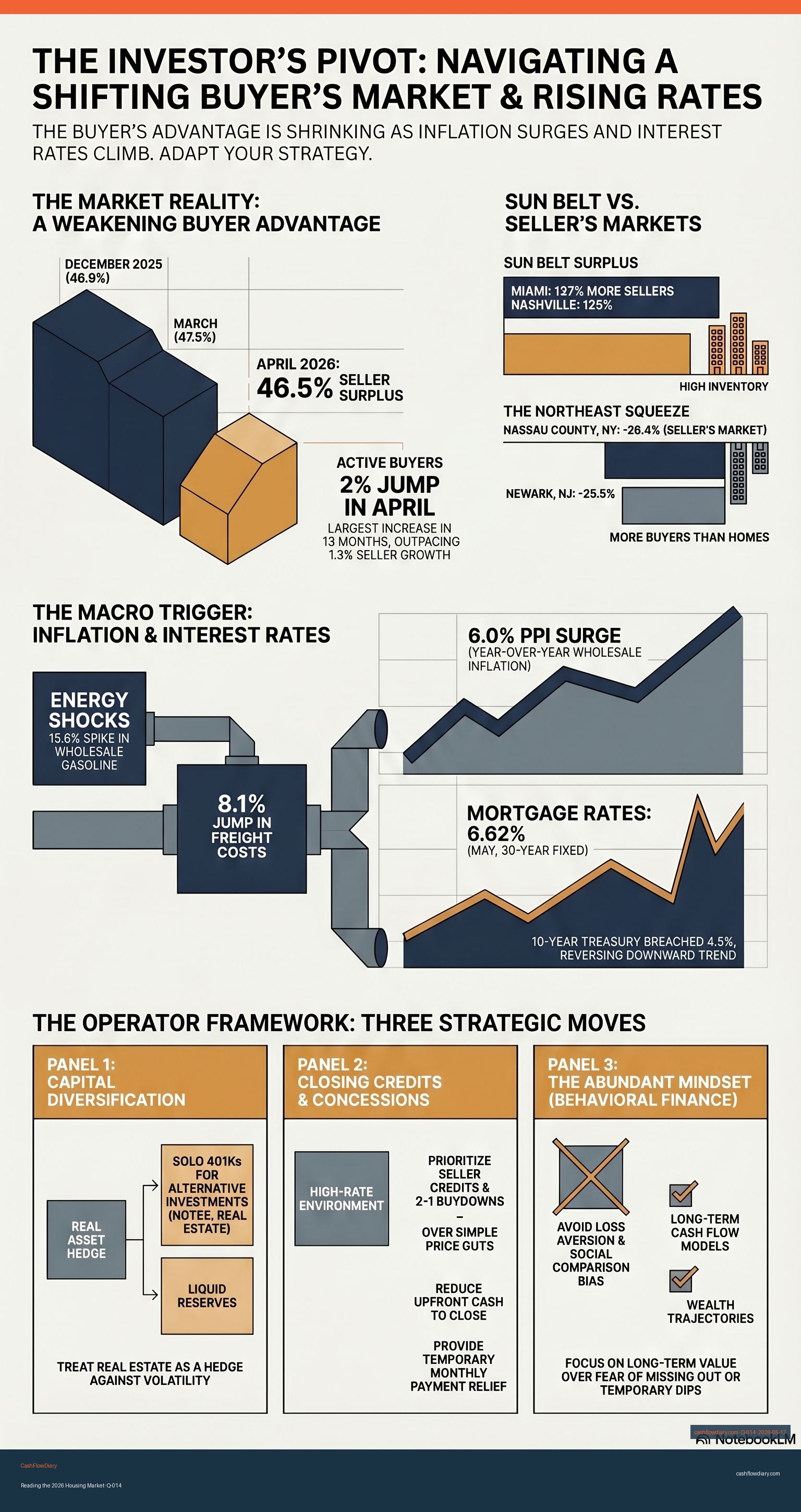

Three weeks ago, the story was that buyers had walked away from the housing market. This week the headline is that sellers outnumber buyers by 46.5%, the largest imbalance in three years — and the Producer Price Index just spiked at the fastest monthly pace since 2022, pushing the 30-year mortgage rate to 6.66%. Both of those things are true at the same time. If you wait for them to agree, you will be waiting forever.

If you needed groceries, would you sit in your house with the keys in your hand until every traffic light between you and the store turned green? No. You would drive. You would use the brakes, the seat belts, the turn signals, and the rules of the road. You would not be reckless, but you would not be frozen either, because you trust that you can get to the store. Most aspiring real estate investors right now are sitting in the kitchen waiting for green lights.

This article is about how to drive.

What Most Real Estate Investors Get Wrong About Mixed Data

Mid-May 2026 produced two reports that contradicted each other if you read them like headlines. Redfin published its April buyers-vs-sellers data on May 12 showing 46.5% more home sellers than buyers nationally — about one million buyers chasing 1.5 million listings. That looks like buyer leverage. Two days later, the April Producer Price Index came in at 6.0% year over year and 1.4% month over month, the largest monthly jump since March 2022. The 30-year Treasury yield crossed 5% for the first time since 2007. The 30-year fixed mortgage rate closed the week near 6.66%. That looks like a buyer punishment.

Most real estate content will pick one of those two stories and run with it. The investor reading the picked story freezes, because the picked story does not match what the investor sees in the next news cycle, and that mismatch reads as "I don't have enough information yet."

This is not an information problem. It is a framework problem.

When you are on the buy side of any transaction, you are dealing with fear. When you are on the sell side, you are dealing with greed. When we procrastinate on the buy side, it is almost never because we lack the data. It is because we believe the outcome will not be in our favor more than we believe it will be. If we knew, beyond every shadow of a doubt, that the outcome would be in our favor, we would move. Not recklessly — with the brakes, the seat belts, the turn signals — but we would move.

The reason most investors freeze right now is not the data. It is the absence of a framework for how to read contradictory data. So let me give you one.

The CFD Perspective: Why Most Operators Only See One Capital Source

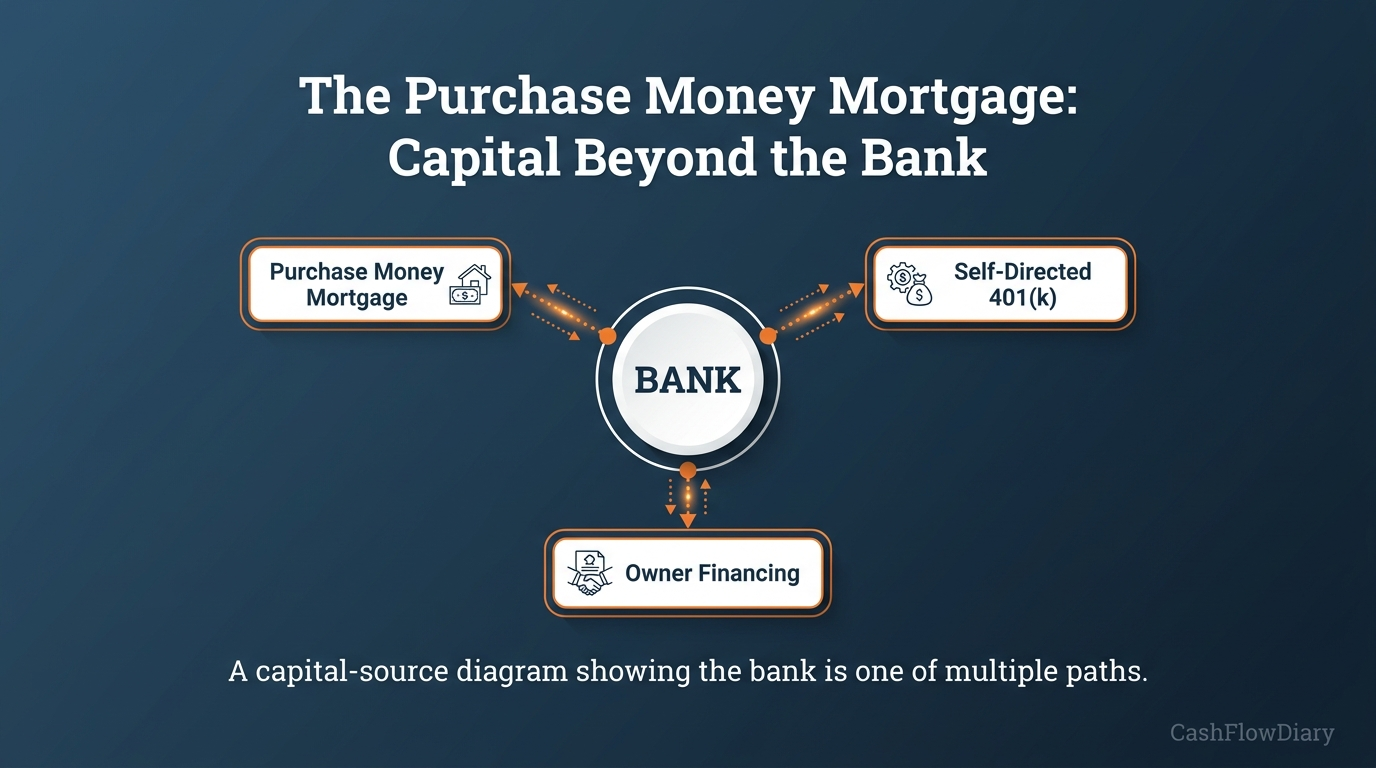

Here is the actual issue most aspiring investors run into. It is not that interest rates are doing whatever they are doing. It is that they need a bank's money in order to purchase a property, and they do not have another method for acquiring the property without the bank being involved. So borrowing cost through the bank becomes the variable that controls everything in their mental model — and any movement in that one variable triggers paralysis.

But the bank is one source of capital. There are many more. What you do not know about those other sources can, has, and always will hurt you.

This is not academic. In 2026, the two most operator-relevant alternative sources of capital are purchase-money mortgages and self-directed retirement plans — and both are written into US law and IRS regulations that have not changed in years.

A purchase-money mortgage is a mortgage given by the buyer of real property to the seller of that property as part of the transaction, in place of paying the full price in cash. The Cornell Legal Information Institute puts it cleanly: the seller finances a portion of the sale by accepting a mortgage from the buyer instead of receiving the full purchase price at closing. The terms — interest rate, repayment schedule, balloon timing — are negotiated between the two parties and can look nothing like a traditional bank mortgage. The technical term Investopedia and most lenders use for the same thing is also "purchase-money mortgage," sometimes called owner financing or seller financing. Several variants are well-documented: SoFi's explainer catalogs land contracts, lease-purchase agreements, lease-option agreements, and assumable mortgages, all of which fit under the purchase-money umbrella.

"When you're on the buy side of any transaction, you are dealing with fear. When you're on the sell side, you are dealing with greed. The reason most investors freeze right now is not the data — it is the absence of a framework for how to read contradictory data."

— J. Massey · CashFlowDiary

The second source is the self-directed 401(k), which by the time you read this is the single largest pool of capital that most operators do not know they have access to. Other people's retirement money — properly structured under IRS Section 4975 — can fund real estate purchases inside a tax-advantaged wrapper. The trick is that the IRS prohibited transaction rules are strict about who can transact with the plan: you, your spouse, your lineal ascendants and descendants, and any entity 50% or more owned by any of the above are all disqualified persons. The plan can buy real estate, hold notes, partner with non-disqualified investors. It cannot buy your house, rent to your child, or pay you for sweat equity on a property it owns. Solo 401(k)s have one additional structural advantage over self-directed IRAs: they are exempt from Unrelated Debt-Financed Income tax on leveraged real estate, which matters a great deal when the plan finances a property through a non-recourse loan.

As Daryl Fairweather, PhD, Chief Economist at Redfin and a behavioral economics PhD from the University of Chicago, observed in March: "Because this data is seasonally adjusted, the record gap tells us this isn't just a seasonal pattern — it reflects a deeper pullback in buyer demand driven by high costs and economic uncertainty."

That deeper pullback is the bank-buyer flinching at the rate. It is not the entire investor universe flinching. Operators who underwrite with a wider capital toolset are not in that pullback at all. They are reading the same data and seeing a different deal.

What To Actually Do When the Data Contradicts Itself

If you accept that the freeze is a framework problem and not an information problem, the question stops being "should I buy?" and becomes "given that I am going to act, how do I act in a way that is safe?"

Three operator moves.

Capital diversification before any deal. Before you write the first offer, know your sources. A purchase-money mortgage requires a seller who owns the property free and clear, or close enough to it, and who is open to financing some or all of the sale price. A self-directed 401(k) requires the right plan structure — not every plan administrator allows real estate, and "checkbook control" is a setup detail that has to happen before the deal, not after. The operators who close deals in 2026 already know which of these sources their next purchase will rely on, in what proportion, before they call the listing agent.

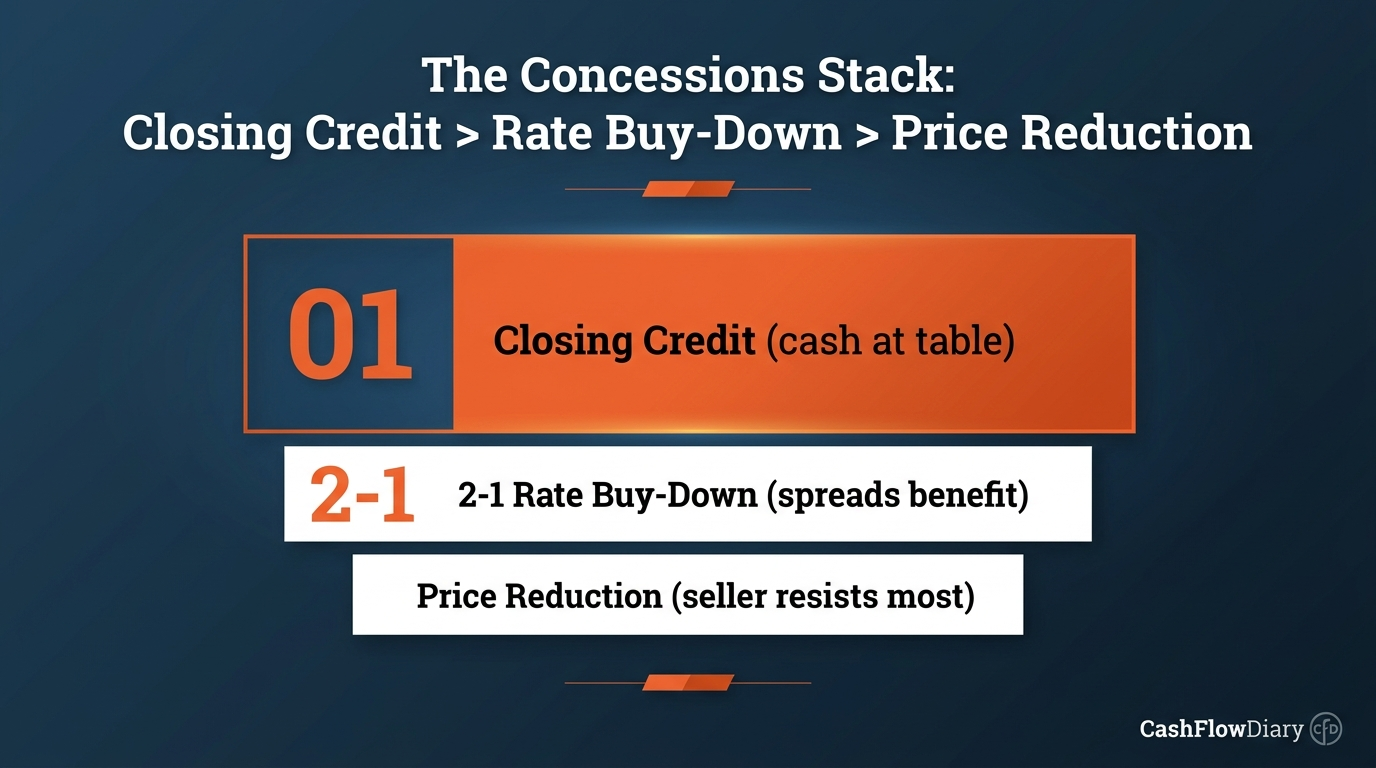

Negotiation: closing credits outperform rate buy-downs and price reductions. Here is the contrarian point. Almost every piece of real estate advice you will read in 2026 will tell you to negotiate either a price reduction or a temporary 2-1 rate buy-down. The right tool is usually neither. A rate buy-down spreads its benefit over the first one or two years, which is real but limited and which the buyer must qualify at the full note rate anyway. A price reduction is the thing the seller fights you on the hardest because it directly hits their headline number and the appraisal comp. A credit at closing — a cash contribution from the seller toward your closing costs or buyer-funded buy-down — solves your actual problem, which is the cash you need at the closing table, and the seller resists it less because the headline price stays where they want it. JVM Lending's analysis is worth reading on the federal limits: closing cost contributions are capped at 3%, 6%, or 9% of the purchase price for Fannie Mae and Freddie Mac loans depending on your down payment, 6% for FHA, and 2% for investment properties. Inside those caps, the credit is a more flexible negotiation tool than either of the alternatives.

Posture: abundance, not urgency. The 46.5% number tells you that there are many more sellers than buyers right now. So whether the imbalance is "real" or a head fake is not the question. The question is, are you willing to buy? There are people who need clean, safe, affordable housing, and there are many of them. There are sellers who need and want to sell, and there are many of them. What this signals is that you do not have to feel pressure to buy any one particular property, because there is another seller around the corner. The investor who walks into negotiations with that posture — calm, abundant, willing to walk — gets terms the urgent investor does not.

As Asad Khan, Senior Economist at Redfin, noted in Redfin's May press release: "Homebuyer demand has been dwindling for months, but finally ticked up in April thanks to a strengthening job market and declining recession risk. More house hunters entering the market helped narrow the gap between the number of buyers and sellers."

Buyer demand ticked up by 2% in April, the largest monthly increase in 13 months. The peak of the buyer's market may already be behind us — meaning the imbalance number you are reading today is the most operator-favorable it is going to be for a while. That is the signal. It is not "wait for clarity." It is "the window is open and starting to close, and the operators who built their capital framework already are walking through it."

If you are currently under contract on a property, this is not the week to renegotiate anything. The data did not tell you to. What you should do is keep your abundant mindset intact through your due-diligence period. If due diligence surfaces something — a roof issue, a foundation crack, an inspection finding — you renegotiate then, on the inspection finding, not on a Redfin chart. Renegotiation triggers off of due diligence, not off of headlines.

FAQ

Is 2026 a buyer's market or a seller's market?

By Redfin's definition — sellers outnumber buyers by more than 10% — the United States is still in buyer's-market territory. The 46.5% imbalance in April 2026 is large. But it is down from a peak of 48.9% in December 2025 and from 47.5% in March, and buyer demand rose 2% month over month in April. The market is buyer-favorable and softening from peak buyer leverage. For most operators, that is the most actionable reading.

Should I buy a house now or wait for mortgage rates to drop?

Waiting for rates to drop assumes you know which direction rates will move next. Through May 2026, rates moved in the opposite direction from what most forecasters predicted at the start of the year. Bond markets repriced after the April Producer Price Index print, Treasury yields crossed 5% for the first time since 2007, and the implied probability of a Federal Reserve rate cut by year-end fell sharply. If your only acquisition path is a 30-year conventional bank mortgage, you are betting your timing on a variable that has not behaved as expected for over a year. If your acquisition path includes a purchase-money mortgage, a self-directed 401(k), or a closing credit that buys down the early years, your timing depends much less on the variable you cannot control.

What seller concessions can I ask for in 2026?

The most flexible concession is a credit at closing, which solves the buyer's cash-to-close problem and faces less seller resistance than a price reduction. The federal contribution caps are 3-9% for Fannie Mae and Freddie Mac (depending on down payment), 6% for FHA loans, and 2% for investment properties. Inside that cap you can route the credit toward closing costs, prepaid taxes and insurance, or a temporary rate buy-down — whichever solves your specific constraint. Temporary buy-downs (2-1 or 3-2-1) can only be seller-paid, not buyer-paid, which is the inverse of permanent buy-downs.

What does the Producer Price Index have to do with my mortgage rate?

The Producer Price Index is the wholesale-side cousin of the Consumer Price Index. When PPI jumps 1.4% in a month, the bond market reads that as a leading indicator that retail inflation has another leg up coming. Bond traders sell Treasuries when they expect inflation, which pushes Treasury yields up. Mortgage rates are priced off the 10-year Treasury plus a spread. So when wholesale prices surge — as they did in April 2026 — the chain runs PPI to Treasuries to mortgage rates within days, regardless of what the Federal Reserve decides to do at its next meeting.

Where can I read more on the framework?

For the housing demand side, the companion piece on pending home sales covers what the supply-and-demand data looks like from a different angle. The free CashFlowDiary newsletter sends one operator framework per week.

Sources

• Redfin · America's Housing Market Favors Buyers — But Their Advantage Is Finally Starting to Shrink

• Redfin · The Housing Market Favors Buyers — But Their Advantage Is Shrinking

• National Apartment Association · Inflation Insights May 2026

• BytePith · US PPI Surges 1.4% in April 2026, Fastest Since 2022

• REI Prime · Rate-Hike Odds Jump to 28% as PPI Hits 6.0%

• Cornell LII · Purchase-Money Mortgage

• SoFi · Purchase-Money Mortgage: Definition and Example

• Investopedia · Purchase-Money Mortgage

• MySolo401k · Prohibited Transactions Self-Directed 401k

• Mission Wealth · The Psychology of Buying a Home (Behavioral Finance)

• JVM Lending · Seller-Paid Temporary Buydowns vs. Seller-Paid Closing Costs

• Available Max · Seller Concessions in 2026: Credits and 2-1 Buydowns

• Real Estate News · Sellers Outnumber Buyers by Largest Margin in Over a Decade