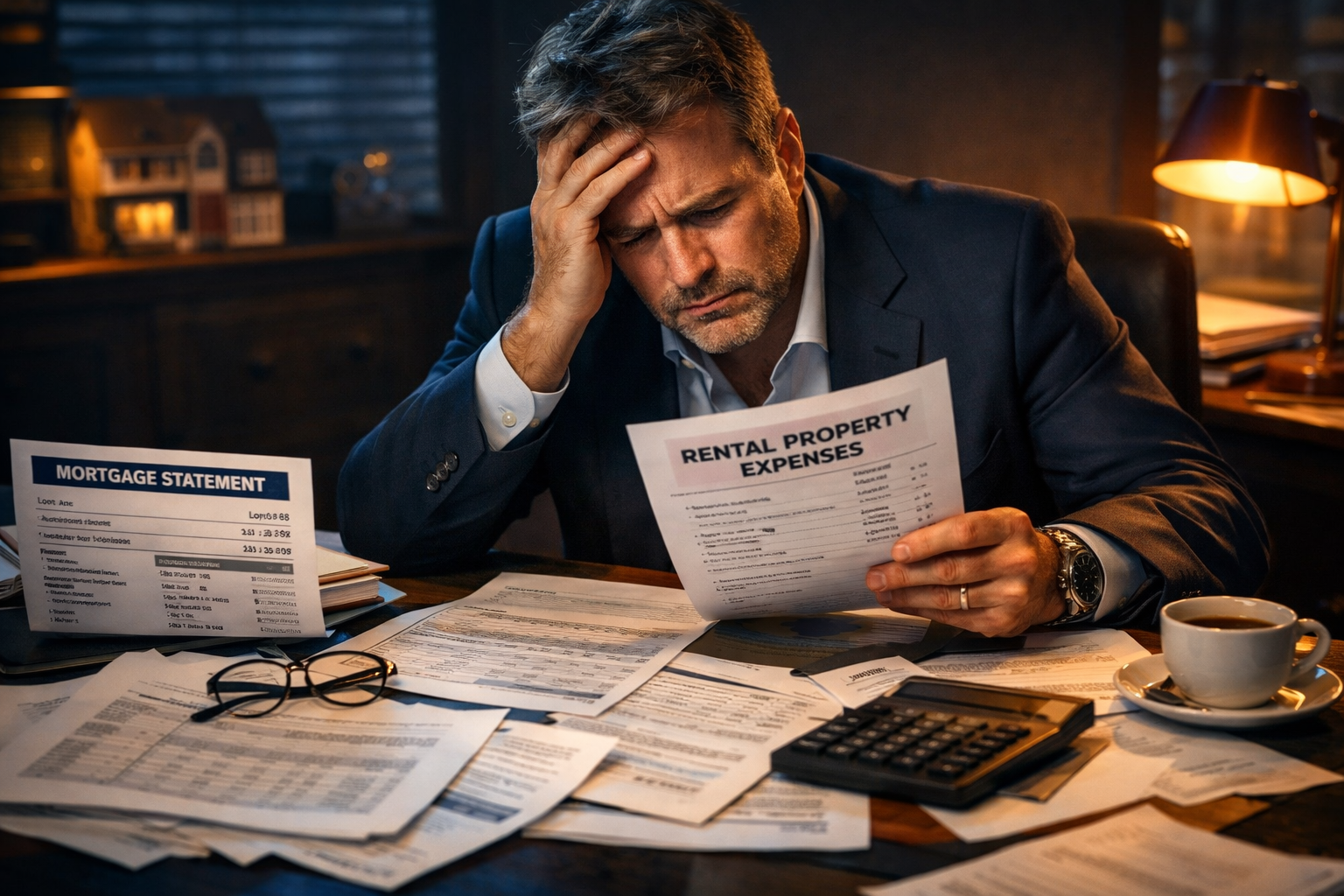

Your first rental property went well. You ran the numbers, found the deal, signed the lease, got your first guest. The confidence that followed was real.

Then you moved to the second one. And suddenly everything is hitting at once.

The to-do list is longer. Unexpected expenses keep showing up. Your cash reserves are stretched from property one, and property two needs work you can’t afford to rush. An investor on Reddit described this exact experience last week: they’d already drained their cash paying off a boiler debt on the first property, and now the second one needed everything at the same time. They were thinking about selling it just to get relief.

Here’s what that Reddit thread didn’t say: this isn’t a you problem. This is what scaling through property ownership feels like. And there’s a different path.

The Real Reason Your Second Property Feels Different

Your first property worked because you had one thing your second one lacks: margin.

On property one, you had time, cash reserves, and the ability to absorb surprises. By the time property two arrives, you’ve already deployed that margin covering property one’s problems. You start property two with less runway than you had at the start. The math on that is brutal.

Property one didn’t test your systems. Property two does. This isn’t about whether you bought a bad deal. It’s about what owning real estate at scale actually requires: capital reserves for every unit, maintenance buffers, and carrying costs that compound as your portfolio grows.

The Cash Flow Trap That Catches Most Investors at Property #2

Here’s the math most investors skip.

If property one ties up $40,000 in capital — down payment plus reserves — and property two needs another $40,000, you’ve deployed $80,000 before you’ve stabilized income from both. Add an unexpected boiler, a vacant month, or a roof repair you didn’t budget for, and the number climbs. Every new property you acquire through ownership adds another mortgage payment, another insurance premium, another reserve account, another lender who needs to see your debt-service coverage ratio before they’ll talk to you.

This is why most investors stall between unit one and unit three. It isn’t motivation. It’s math.

What the Reddit Thread Got Right (And What No One Mentioned)

The investor in that thread described the feeling precisely: the first property built their confidence, and the second one was testing it. They were seriously considering selling property two and using the proceeds to pay down property one faster.

That’s not a strategy. That’s a liquidity squeeze looking for an exit.

What the thread didn’t surface: there’s a model that lets you scale STR income without the balance sheet weight of ownership. You don’t have to own a property to operate one. And you don’t need another mortgage to build another income stream.

It’s called rental arbitrage. And it’s how thousands of STR operators have built $3,000 to $10,000 per month in cash flow without a single down payment.

How Rental Arbitrage Solves the Scale Problem

Rental arbitrage means you lease a property from a landlord at a fixed monthly rate and host short-term or mid-term guests at nightly or weekly rates. You keep the spread between what guests pay you and what you pay the landlord.

No mortgage. No property tax. No CapEx reserve for a roof. You’re operating a hospitality business inside a lease agreement.

Here’s how the capital picture compares:

Property ownership: $20,000–$60,000+ to enter one unit (down payment, closing costs, reserves)

Rental arbitrage: $3,000–$8,000 to enter one unit (first/last month rent plus furnishings)

Scaling to 5 owned units: $150,000–$300,000+ in capital required

Scaling to 5 arbitrage units: $15,000–$40,000 in capital required

You can build five arbitrage units for less than the down payment on a second owned property. That’s not a workaround. That’s the model.

The Numbers: What Rental Arbitrage Actually Earns

You lease a 2-bedroom in a steady market for $1,800/month. On Airbnb or Furnished Finder, the same unit books at $100–$160/night. At 65% occupancy — roughly 20 nights per month — you bring in $2,000–$3,200 in revenue. After rent, cleaning fees, platform costs, and supplies, your net is $300–$1,000 per month per unit.

Three units at that level generates $900–$3,000 per month in net income — without buying a single property, without a mortgage application, without a debt-service calculation.

The KNOW / DO / TRACK Framework for Your First Arbitrage Unit

KNOW:

Property ownership at scale requires capital that compounds with every unit added

Rental arbitrage scales with lease agreements instead of mortgages

You need one thing to start: a signed lease that permits subletting for short-term guests

DO:

Find 3 landlords in your target market with vacancy issues who want reliable long-term tenants

Propose a managed sublease: guaranteed rent plus professional management of the unit

Sign a lease that explicitly permits short-term hosting — get this in writing before furnishing anything

Furnish for $3,000–$8,000 using Facebook Marketplace and IKEA. Functional and clean beats new

List on Airbnb and Furnished Finder the same week. Target your first booking within 30 days of signing

TRACK:

Monthly net cash flow per unit (revenue minus rent, cleaning, platform fees, supplies)

Occupancy rate (target 60–65% in your first 90 days as reviews accumulate)

Average daily rate (watch this climb as your review count passes 10, then 25)

What to Do Right Now

If you’re at property one and already dreading property two — stop. You don’t have to acquire another property to scale your STR income. If you’re already at property two and feeling the cash squeeze, the arbitrage model doesn’t require you to sell anything. It runs alongside your owned properties with a separate capital pool and a different risk profile.

The STR Blueprint walks you through every step: finding landlords open to managed sublease arrangements, structuring the agreement, furnishing for profit, and booking your first guest. It’s the same system J. Massey used to build a portfolio of STR units without owning the properties underneath them.

Your second rental property feeling impossible isn’t a sign you should stop. It’s a sign the ownership model has real limits — and you’ve just reached them. The question is whether you want to keep pushing against those limits or step around them entirely.