The Paycheck Trap: Why Trading Time for Money Keeps You Stuck (And the Sequence That Breaks It)

51% of Americans live paycheck to paycheck — but the problem isn't money, it's sequence. Invert the order: learn to make property produce cash flow before you take on the debt.

Disclosure: This post may contain affiliate links. If you purchase through our links, we may earn a commission at no extra cost to you. We only recommend tools and services J. Massey's team actually uses.

Learn more →

TL;DR: 51% of Americans live paycheck to paycheck, but the problem isn't money. It's sequence. The standard path (job, save, buy property, then learn to operate it) destroys liquidity before you build skills. Inverting the sequence (arbitrage first, ownership second) lets you learn how to make property produce cash flow before you take on debt. Build operational fluency with income instead of risk.

The core fix:

Standard sequence destroys liquidity and traps you in time-for-money exchanges

Rental arbitrage lets you learn property operations without ownership risk ($5K-$15K startup vs. $50K+ down payment)

Build systems across three properties on someone else's balance sheet, then buy property one with proven operations

Deploy automation (guest comms, review responses, weekly reviews) before property three or the wheels come off

Interactive · run your own numbers

When does an arbitrage unit pay you back?

$2,200

$180

70%

$10,000

Monthly profit

$1,330

after lease + ~25% opex

Months to recoup setup

7.5

then it's pure cash flow

First profit lands in

Month 2

Compare that to 18+ months for new-build ownership.

I've spent 15+ years in this space, trained more than 10,000 operators through CashFlowDiary, and recorded 237+ podcast episodes breaking down the deals that work and the ones that don't. The pattern below shows up in every cycle.

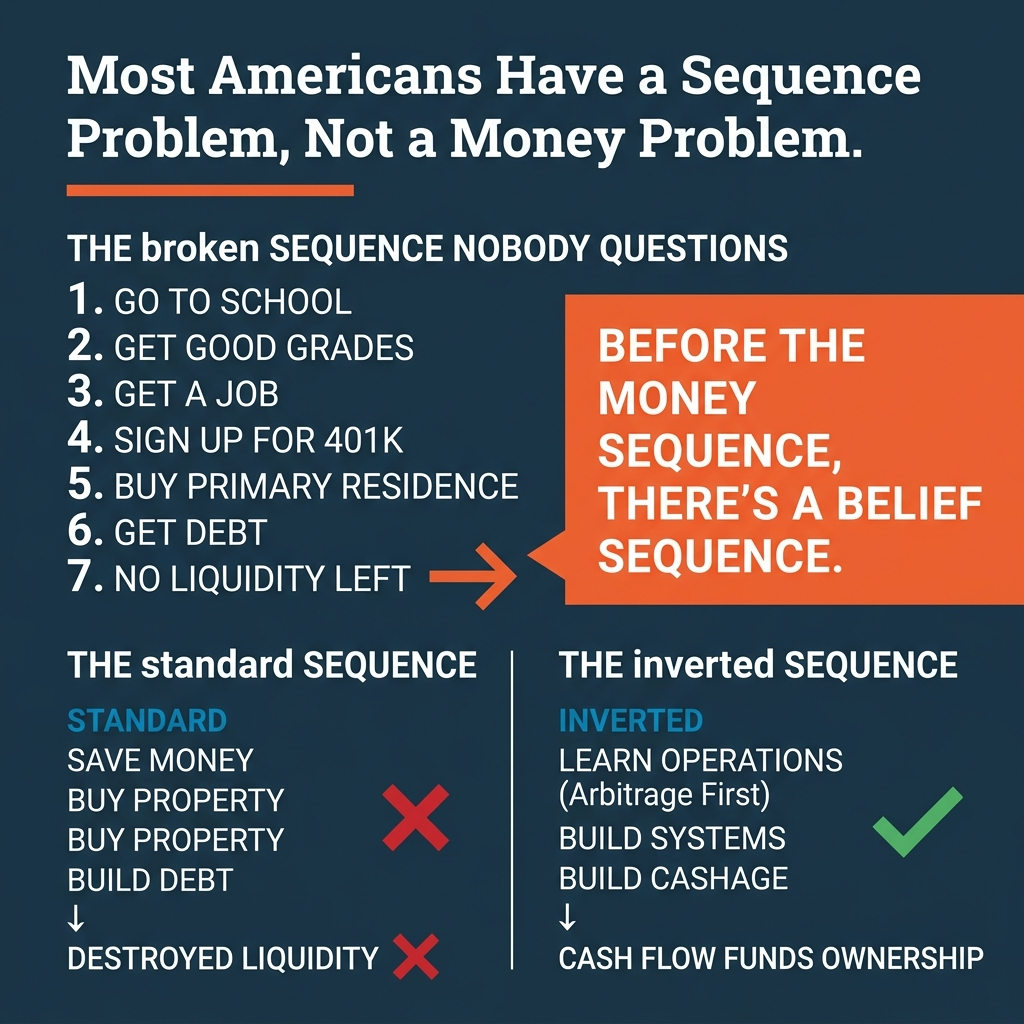

Why 51% of Americans Are Trapped

Standard sequence vs inverted sequence — job-save-buy-learn vs arbitrage-learn-buy

The problem has three layers: what you believe about money, how you earn it, and what you do with it once you have it. Fixing layer three (spending habits) while ignoring layers one and two (belief systems and earning structure) changes nothing.

"The problem isn't money. It's sequence. Learn to make property produce cash flow before you take on the debt — not after."

— J. Massey · CashFlowDiary

The Standard Sequence Nobody Questions

Here's the path most people run without ever being asked if they want to:

School. Good grades. More school for some, which adds debt. Then the job. Someone tells you to sign up for a 401k, so you do. You want a house. You get the spouse, the kids, the dog, the picket fence. You start thinking about retirement. Somewhere in there, you realize your liquidity is gone.

Owning your primary residence too soon destroys liquidity. Investing in a 401k destroys liquidity. Tying income directly to labor in a one-to-one ratio compounds the problem. Now you're on credit cards running on compound interest while nothing else you own earns any interest. You're trying to keep up, and it's all connected to labor. You feel stressed. You send your spouse to work. Now there are two stressed people who need to figure out whose turn it is to do the dishes.

Running these steps out of sequence creates a liquidity problem, which creates a debt problem, which prevents you from investing in your future because you're too busy paying for the past.

Key point: This isn't personal failure. It's what happens when you run the sequence in the wrong order.

Why Time-for-Money Has a Ceiling

Every dollar you earn costs you time. You show up, you produce, you get paid. The equation feels like progress because the number goes up when you work more.

Time is finite. Whether you're paid $15 or $150 per hour, your income is capped by hours available. There are 24 hours in a day. You need eight to sleep, two to commute. That leaves 10 to 12 hours to trade for income. No matter how much your time is worth, there will always be a ceiling imposed by the clock.

The real cost shows up when you take time off. When you make money from selling time, taking time off has a price. You don't make money unless you're working. The vacation costs you twice: once for the trip, once for the income you didn't earn while you were gone.

Hours preparing. Hours in traffic each way. It's on your mind after hours. Ask yourself: if the same dollars came in from assets instead of your labor, what changes? Those same 160 hours a month could go to something different. Same income. Different source. That shift alone changes quality of life before you ever earn an extra dollar.

Key point: The ceiling isn't personal failure. It's the model.

Asset Owners vs. Income Earners: The Widening Gap

Here's what separates the two:

Income earners trade time for money. Asset owners let the asset produce income while they're not in the room.

Asset growth outpaces income in most markets. When real estate or stocks grow faster than what you earn from labor, asset owners build wealth while income earners fall behind.

The ratio of median house prices to median household incomes climbed from 3.5 in 1985 to 5.1 in 2025. The median cost of a house grew to over five times the median annual income of a household. If you're trying to save your way into ownership from a paycheck, the finish line is moving faster than you are.

Ownership allows wealth to compound faster than wages over time. $100,000 worth of stock grows tax-deferred and keeps compounding without getting clipped unless you sell it. Your paycheck gets taxed before you see it, taxed again when you spend it, then clipped by inflation while it sits in your account.

Piles of cash don't work in an inflationary economy without sound money. Saving up isn't the path to retirement. It's the path to a big purchase. What gets you to consistent income with less labor over time is assets. Nobody told you that. They told you to save. Most of us swallowed that pill and wonder why we feel sunk.

Key point: The system is built to favor asset owners. If you're still trading time for money, you're playing a game the rules don't support.

The Belief Sequence Comes First

Here's what most financial advice skips.

To own an asset, you need three things: correct mindset, correct skillset, correct toolset. The toolset is easy. You buy it once you have capital. The mindset is harder. The skillset is hardest because you have to sustain the right mindset while you're learning something new. That's when most people quit.

You cannot behave consistently in ways that are inconsistent with who you believe yourself to be. Every person has a powerful belief mechanism, and it shapes everything. When you believe an outcome is in your favor, you act differently than when you believe it isn't. Same information. Different frame. Different outcome.

Two people look at the exact same opportunity (same math, same market, same starting point) and one sees a path while the other sees a trap. The variable isn't the opportunity. It's the frame.

Most people in the sequence trap aren't there because they made bad decisions. They made the decisions they were told to make, in the order everyone around them endorsed. The belief sequence was set before they ever had a choice. School is the path. The job is the goal. The 401k is the plan. Question any of it and you're being irresponsible.

Key point: The first thing that has to shift isn't your strategy. It's your frame. You have to be open to earning income in a different way, because the way you've been doing it hasn't been working. Most people will defend the sequence that's trapping them before they'll question it, because questioning it means admitting the last ten years were spent running in the wrong direction.

The Standard Sequence Destroys Liquidity Before You Build Skills

Most people don't have a money problem. They have a sequence problem.

The standard sequence: get a job, save money, buy a property, figure out how to manage it. That order destroys liquidity before you have any skills.

They've destroyed their liquidity and ability to access cash, which is why they end up with credit cards. By the time they buy the property, they're leveraged, they're learning on the job, and every mistake costs them real money because they own the asset.

Here's what nobody explains clearly: to make real estate work, you need four ingredients: knowledge, time, money, and credit. Most people stop at "I don't have money or credit" and treat that as the end of the story. They don't focus on what they do have: knowledge and time.

You only need to bring one ingredient to the table. One. If you have knowledge and time in sufficient quantity, you leverage those to access someone else's money and credit. The inverse is also true: if you have capital, you leverage someone else's knowledge and time. The ingredient you have is enough to get started. Most people never reach that conclusion because they're too focused on what's missing.

Key point: Buying a short-term rental property in 2026 requires a $50,000+ down payment, a 6.22% mortgage rate, and a long-term commitment to a single asset. Most people building STR portfolios from scratch won't do that. The inverted sequence (arbitrage first) solves that problem.

Arbitrage First: The De-Risked Path

A time-for-money hamster wheel hitting an income ceiling

Rental arbitrage means you lease a property long-term and rent it out short-term. You're not buying. You're operating.

Startup costs are $5,000 to $15,000 per unit, compared with $50,000+ for a purchase. You're learning how to make a property produce cash before you take on the full expense of ownership.

Here's what you're outsourcing to the property owner while you lease:

Random large-ticket expenses. The HVAC dies, the roof leaks, the water heater fails. That's the owner's problem, not yours. You don't realize how many random large-ticket expenses you're outsourcing to the owner of the property while you're leasing it.

Market risk. If demand shifts or the market changes, you end your lease after its term and move on. You're not tied down to a property as you would be with ownership. You test different locations with less risk than owning property in a declining market.

Operational learning curve. One of the biggest de-risks is you get the experience of finding the customer, getting rid of bad customers, and developing all of the processes to then find another customer. You're building the system on someone else's balance sheet.

By inverting and going with arbitrage first, you get to figure out how to make a property make money before you have to take on the full expense.

Key point: Average rental arbitrage profit in markets like Oklahoma City is $800 to $1,500 per month per property. That's real cash flow. If you run three properties on arbitrage, that's $2,400 to $4,500 per month. That's not replacing a six-figure income, but it's decoupling time from money for the first time.

What This Looks Like in Practice

I'll give you the concept first, then the proof.

You lease a 2-bedroom apartment for $1,500 per month. You furnish it, list it on Airbnb, and earn $2,500 per month from short-term guests. Your gross profit is $1,000.

You're not rich. But you're learning:

How to find the property that works for short-term rentals

How to price it so it stays occupied

How to automate guest comms so you're not answering messages at 11pm

How to build a cleaning system that doesn't require you to show up

How to handle bad guests without losing your mind

How to run the operation so the property produces cash whether you're in the room or not

You're building operational fluency with income, not debt.

Now the proof.

I started in real estate with no money and no credit. I was squatting in a bank-owned property. I had a hole in my lung. I couldn't walk and talk at the same time. I needed a way to eat without being able to go to work, so I started selling personal possessions on eBay until the closet was empty, then started buying from garage sales and selling other people's possessions. I didn't realize I was learning wholesaling. That's how I got started.

Then I got the bird flu. I went to the hospital. When I came back, my ex-wife had taken the kids and left because I was contagious. I was bedridden, in and out of consciousness, watching B-roll movies on Netflix. In my few lucid hours, I was still processing wholesale transactions. Something became clear: there was only a very small part of the transaction that I personally needed to participate in. Systems were running in the background. Even while I was sick, I closed three or four transactions and made more than what some people earn in a month.

That moment taught me a job wasn't necessary. Finding something of value in the marketplace, finding those who value it, connecting the two: that was the value I could create. And I could do it in less than an eight-hour day. The system ran without me. Once you see that, you can't unsee it.

The feeling was mixed. There was anger (why wasn't I told this before?) and relief (I found a solution). Both at the same time. Because when you realize what you thought was true isn't true, it raises a harder question: what else might not be true? And why didn't anyone tell you sooner?

Key point: When you buy property number one, you're not guessing. You know what works. You know what the numbers need to look like. You know how to run the operation because you've done it three times on someone else's balance sheet.

That's the inverted sequence.

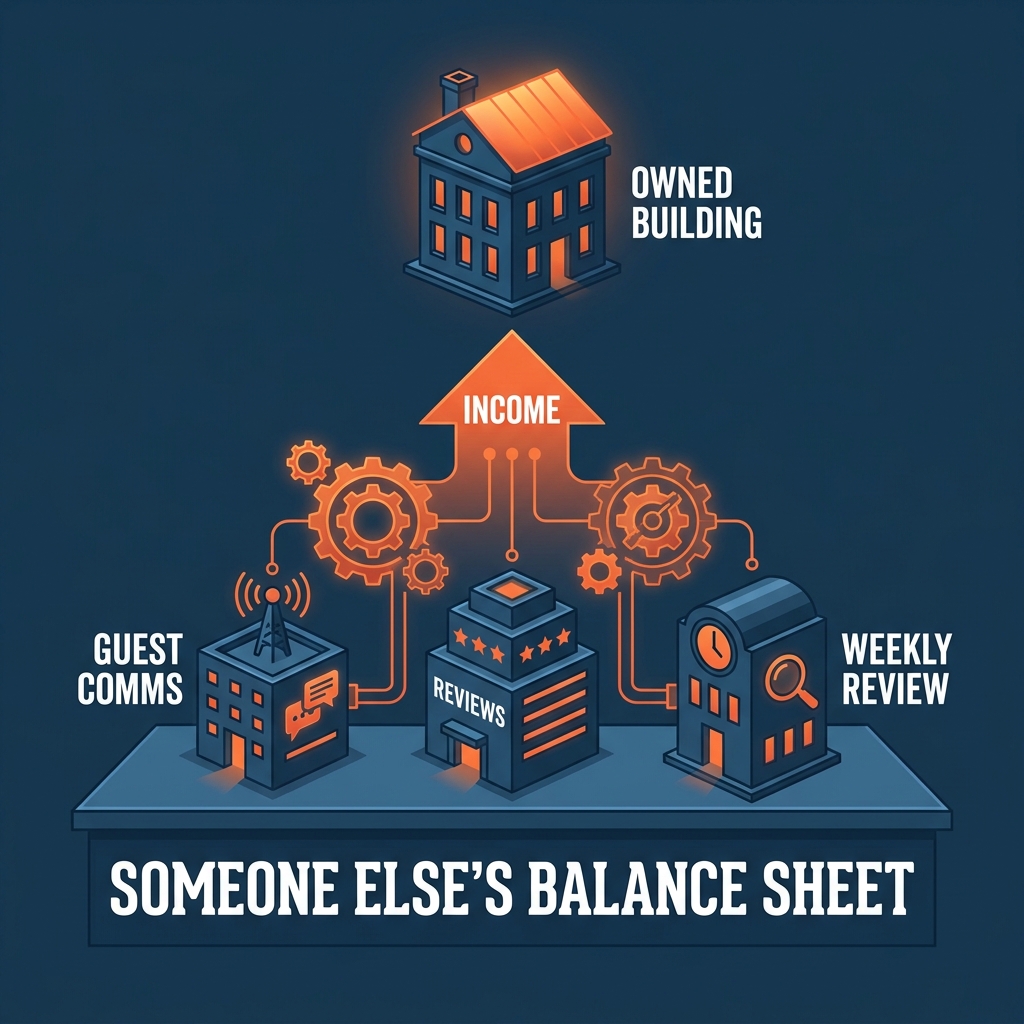

The Three-Property Wall (And How to Avoid It)

Most operators hit the same wall around the third property.

The wall isn't the operations. It isn't capital. It's that you can't run more than two properties out of your head, and most operators try to do exactly that for too long.

The result is predictable: comms slip, reviews drop, the cleaning crew quits on a Sunday, and the operator concludes scaling was a mistake.

The fix isn't more discipline. It's the system you should have built before you launched property three.

Three components, in order:

1. Automated guest comms. Pre-arrival, check-in, during-stay, check-out. The system handles it. You approve exceptions.

2. Automated review responses with a human-approval gate. The system drafts the response. You review and send. Two minutes per review instead of twenty.

3. Friday 30-minute operations review. You review occupancy, pricing, and any flags from the week.

Key point: The first two components take a weekend each to build. The third takes 30 minutes a week, forever. Deploy the first two before you launch property three. The third runs as long as you're operating.

Why Most People Don't Do This

Three properties on someone else's balance sheet feeding income via automation

They don't know the sequence exists. And even when they find it, they talk themselves out of it.

Here's the mechanism. The distance between your current reality and what you want is the fuel that moves you. When reality is at zero and what you want is at positive seven, that gap is uncomfortable enough to drive action. But when reality drops to negative seven (the debt compounds, the liquidity dries up, the stress builds) and the desire stays at positive seven, the gap is now fourteen. It doubled. The outcome didn't change. The pain did.

Most people respond to that doubled gap by lowering the desire. They tell themselves they didn't want it. They convince themselves it's not for them, or that they can't see a path, so it must not be possible. They shrink the gap from the wrong end.

That's not a strategy. That's comfort winning over desire.

The standard path is the only path most people see: save money, buy property, figure it out. That order works if you have $100,000 in the bank and six months to learn on the job. Most people don't. The inverted sequence (arbitrage first) removes the capital barrier, outsources the risk, and builds operational fluency before you take on debt.

It's not sexy. It's not "I bought ten doors in my first year." It's "I ran three properties on arbitrage, built the systems, learned what works, and bought property one with cash flow funding the down payment."

Key point: That's the path that doesn't trap you.

What Happens When You Don't Invert the Sequence

You buy property one. You're excited. You're leveraged. You're learning how to run a short-term rental while the mortgage is due every month.

The HVAC dies. That's $8,000. The roof leaks. That's $12,000. The water heater fails. That's $2,500. You didn't budget for those because you didn't know they were coming.

You're three months in and you're bleeding cash. The property isn't producing what you thought it would because you didn't know how to price it, you didn't know how to automate the operation, and you didn't know what good occupancy looks like in your market.

You sell the property or you hold it and bleed for two years while you figure it out.

Key point: That's what happens when the sequence is wrong.

The Next Move

If you're still trading time for money, the next move is to test whether you can decouple the two.

Find one property you can lease long-term and rent short-term. Run the numbers. If the spread is $800+ per month after all costs, you have a working model.

Deploy automated guest comms before you launch. Deploy automated review responses in week two. Run a Friday 30-minute operations review starting in week one.

If the property produces $800 to $1,500 per month and you're spending less than five hours a week on it after month two, you've decoupled time from income for the first time.

That's the test.

If it works, run it again. Property two. Property three. Build the systems so the operations don't require you in the room.

By the time you buy property one, you're not guessing. You know what works. The cash flow from arbitrage funded the down payment. The systems you built on someone else's balance sheet transfer to the property you own.

One more thing. Your outcomes are yours. Not your parents'. Not the economy's. Not the sequence you inherited. We are born looking like our parents. We die looking like our decisions.

Frequently Asked Questions

What is rental arbitrage?

Rental arbitrage is when you lease a property long-term from an owner and rent it out short-term to guests. You're operating the property without owning it, which reduces your startup costs to $5,000 to $15,000 per unit instead of $50,000+ for purchasing.

How much profit does rental arbitrage generate per property?

Average rental arbitrage profit ranges from $800 to $1,500 per month per property in markets like Oklahoma City. Three properties generate $2,400 to $4,500 per month in cash flow.

Why is arbitrage less risky than buying property first?

Arbitrage outsources random large-ticket expenses (HVAC, roof, water heater) to the property owner. You learn operations, customer acquisition, and pricing without the full expense of ownership. If the market shifts, you end your lease instead of being stuck with a depreciating asset.

What systems do I need before property three?

Three systems: automated guest comms (pre-arrival through check-out), automated review responses with human approval, and a Friday 30-minute operations review. Deploy the first two before you launch property three or comms slip and reviews drop.

How long does it take to decouple time from income?

If your property produces $800 to $1,500 per month and you're spending less than five hours a week on it after month two, you've decoupled time from income. The test is whether the property produces cash flow without requiring you in the room.

What's the difference between asset owners and income earners?

Income earners trade time for money. Asset owners let the asset produce income while they're not in the room. Asset growth outpaces income in most markets, which means asset owners build wealth faster than income earners.

Why does the standard sequence (job, save, buy property) fail?

The standard sequence destroys liquidity before you build operational skills. By the time you buy property, you're leveraged and learning on the job. Every mistake costs real money because you own the asset. The inverted sequence (arbitrage first) builds operational fluency before you take on debt.

What do I need to start in real estate?

Four ingredients: knowledge, time, money, and credit. You only need one. If you have knowledge and time, you leverage those to access someone else's money and credit. If you have capital, you leverage someone else's knowledge and time.

Key Takeaways

51% of Americans live paycheck to paycheck because the standard financial sequence (job, save, buy property) destroys liquidity before building skills

Trading time for money has a ceiling: 24 hours a day, minus sleep and commute, leaves 10 to 12 hours to trade for income regardless of hourly rate

Asset owners build wealth faster than income earners because asset growth outpaces wage growth in most markets

Rental arbitrage inverts the sequence: learn to operate properties for $5,000 to $15,000 per unit instead of $50,000+ down payment, build systems on someone else's balance sheet, then buy property one with proven operations

Deploy automation before property three: automated guest comms, automated review responses, and weekly operations review. Without systems, you can't run more than two properties out of your head

The test: find one property to lease long-term and rent short-term. If the spread is $800+ per month after costs and you're spending less than five hours a week on it after month two, you've decoupled time from income

The paycheck trap isn't a money problem. It's a sequence problem. Fix the sequence and the trap doesn't lock

Learn STR Operations the Right Way

Every operator I work with goes through this audit before we build the second channel, the second guest type, the second pricing model. If you want the full framework — the platforms, the compliance sequence, the pricing model that protects margins through regulatory shifts — that's what we map on a strategy call.

Earnings & Income Disclaimer: West Egg Enterprises, Inc. / CashFlowDiary does not guarantee any specific income, profit, or financial results from information on this site. Individual results vary based on effort, experience, market conditions, and other factors outside our control. Past performance does not guarantee future results. Nothing on this site constitutes financial, legal, or tax advice.